The municipal bond market is one of the largest markets in the world, with about $3.9 trillion worth of bonds and about $11 billion in par traded per day.

With their unique tax advantages, many investors use municipal bonds as a way to improve their after-tax returns and generate investment income.

In this article, we will take a closer look at continuing disclosures and how to use them to enhance their due diligence.

Use our Screener to find the right municipal bonds for your portfolio.

Continuing Disclosures

Continuing disclosures are prepared by state or local governments to convey important information about municipal bonds that arise after they are issued.

These disclosures consist of several documents defined in Securities and Exchange Commission Rule 15c2-12 and Rule 15Ga-1, along with certain voluntary disclosures as mentioned below.

- SEC Rule 15c2-12 Disclosures: Issuers must submit these disclosures based on contractual agreements established when a bond is issued.

- SEC Rule 15Ga-1 Disclosures: Municipal securitizers must file these disclosures related to municipal asset-backed securities.

- Voluntary Disclosures: Many issuers make voluntary disclosures that are classified based on the information that they contain.

Investors can access continuing disclosures using the MSRB’s Electronic Municipal Market Access, which can be found here. If you own a specific bond, you can even set up email alerts to keep up-to-date with any continuing disclosures.

What is Contained in Disclosures?

Continuing disclosures can be divided into two categories: financial or operating filings, or event filings.

Financial or operating filings consist of audited financial statements, annual financial information and any notices of failure to provide annual financial agreements on time. These are typically regular disclosures that are made on a periodic basis by issuers to keep bondholders up-to-date.

Event filings notify bondholders of specific events that may affect the repayment of a bond, such as those outlined by the MSRB here.

Some of the key events as defined by MSRB are as follows

- Principle and interest payment delinquencies

- Non-payment related defaults

- Unscheduled draws on debt service reserves

- Unscheduled draws on credit enhancements

- Substitution of credit or liquidity providers

- Adverse tax opinions or changes in tax status

- Modifications to the rights of bondholders

- Bond calls and tender offers

- Defeasances

- Changes to assets securing repayment

- Changes in ratings

- Bankruptcy, insolvency, or receivership

- Merger, acquisition, or sale of assets

- Appointment of a successor trustee

Want to learn how to interpret Credit Ratings for municipal bonds? Click here.

These event filings may influence the valuation of a bond, but they don’t appear for all municipal bonds or issuers.

How Investors Can Use Disclosures

Continuing disclosures are invaluable for investors conducting due diligence on a municipal bond. Without them, investors would be relying on potentially outdated information that could make it difficult to determine if the bond is right for them.

Financial and operating continuing disclosures are helpful for keeping up-to-date with a municipality’s finances. For example, a bondholder may take a look at audited financial statements to determine if there are any changes to the state or local government’s ability to repay the bond.

Be sure to check out our Education section to learn more about municipal bonds.

Event-related continuing disclosures are critical for bondholders to reassess their holdings. For example, a bondholder may receive a notice of a change in credit rating, which could lead them to sell the bond. These disclosures are even more important when it comes to distressed bonds.

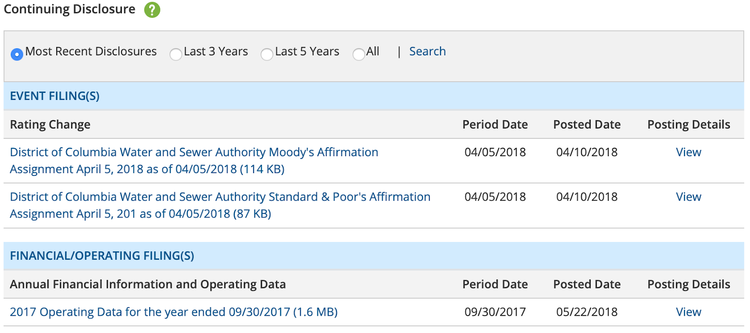

An Example of a Disclosure

Let’s take a look at the District of Columbia’s Water and Sewer Authority Public Utility Revenue Bond (CUSIP 254845AL4) for an example of the kinds of continuing disclosures you may find in the municipal bond market.

The municipal bond issue has had several event filings over the past year. In particular, there have been a number of ratings changes from Moody’s and Standard & Poor’s released each year that could impact an investor’s buying or selling decision.

There were also many financial and operating disclosures, including:

- Annual Financials & Budgets

- Engineering Reports

- Audited Financial Statements

You can find additional examples by searching EMMA’s website for various bond issues using their CUSIP.

The Bottom Line

Continuing disclosures are an important due diligence tool for municipal bond investors. Using EMMA, you can keep up with these disclosures to learn about any changes in financial condition, credit ratings or other factors that could influence the valuation or features of a bond.

Sign up for our free newsletter to get the latest news on municipal bonds delivered to your inbox.