Most investors are aware that they can risk too much, but few realize that playing it too safe also has its own set of risks. By taking on less risk, an investor may compromise their ability to achieve their target performance goal, such as a retirement goal, for their portfolio.

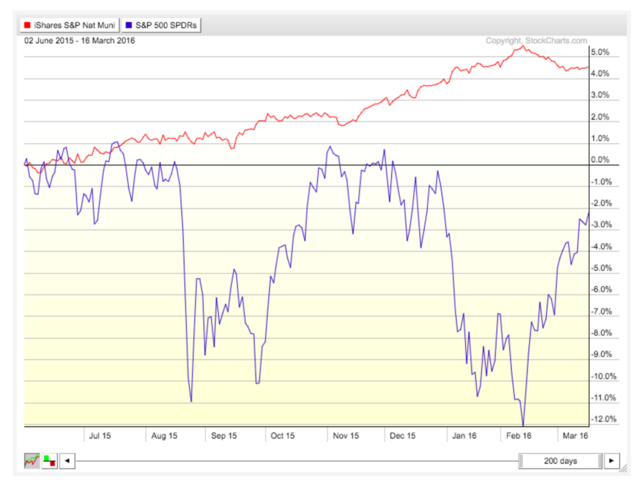

Municipal bonds are widely regarded as a safe-haven asset class since government backing provides better credit ratings than most corporate bonds. Exemptions from federal, state, and local income taxes further create a higher after-tax yield than comparable private-sector bonds. These attributes have helped muni bonds perform extremely well over the past couple of years as investors sought out safe-haven asset classes amid the drop in equity prices.

Below, MunicipalBonds.com takes a look at a few common ways investors may be playing it too safe with muni bonds and some key changes they may want to consider.

Overallocating Muni Bonds

The first mistake that investors often make is overallocating their portfolio to municipal bonds during troubled times in order to reduce their risk.

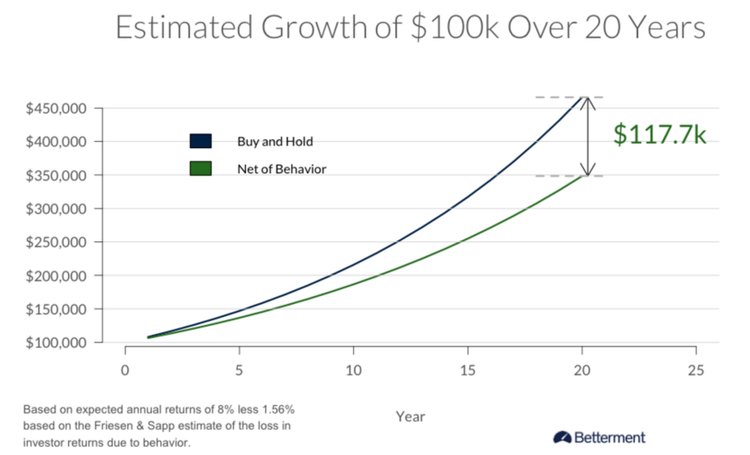

A number of research studies have shown that investors sacrifice between 1.2% and 4.3% of their returns due to attempts at market timing – also known as the behavior gap. According to Betterment’s analysis, investors trying to time the market over 20 years risk losing out on $117,700 in aggregate value for every $100,000 invested over the time period. This calculation was made using one of the more conservative estimates of 1.56%.

Investors may be tempted to overallocate their portfolio to muni bonds during an economic downturn, but doing so could cost them money over the long run. Often times, it’s a much better idea to keep a steady allocation that is set up to meet a target goal over time rather than trying to time the market and avoid losses. Research suggests that few people are able to do the latter successfully over the long term.

Short-Duration Mistakes

The second mistake that investors often make is focusing on short-duration municipal bonds during troubled times in order to reduce their risk.

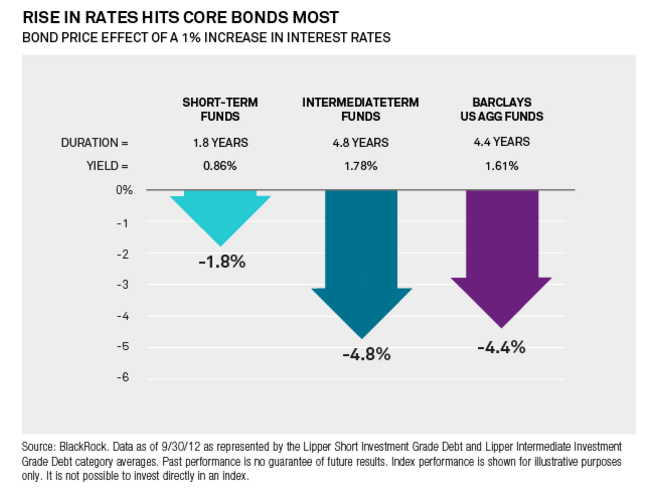

Duration is an important measure of risk when it comes to all types of bonds, including muni bonds. It’s a measures of how long, in years, it takes for the price of a bond to be repaid by internal cash flows. Bonds with longer durations carry greater risk and experience more price volatility than bonds with shorter durations. After all, longer durations mean that bondholders are tied to the bond’s interest rate over a longer period of time.

The problem with moving into short-duration as a safer investment than longer-duration muni bonds is that there’s an increased reinvestment risk. In other words, an investor may not be able to reinvest the proceeds of a short-term bond into a comparable bond when it matures. Longer-duration muni bonds have lower reinvestment risk because there’s a longer period of time before the bond matures and the interest rate differential may be minimal.

The Bottom Line

Most investors are aware that their portfolio can be too risky, but playing it safe has its own costs. Often times, investors purchase short-duration municipal bonds as a safe-haven asset. Market timing has a long-term cost known as the behavior gap, while short-duration bonds may pose a reinvestment risk. Investors should carefully consider these risks when evaluating muni bonds – especially during an economic downturn.